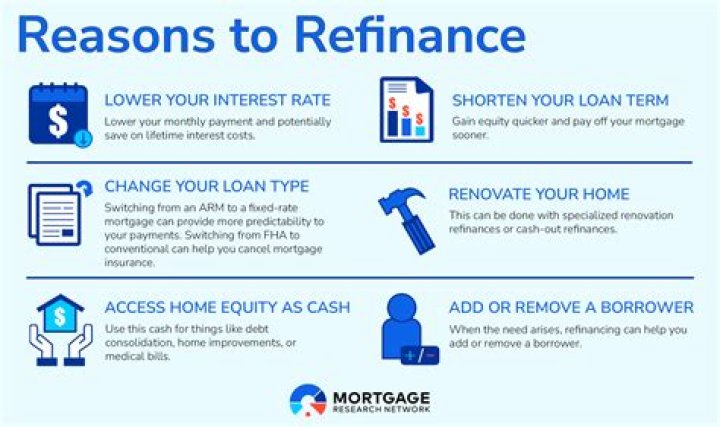

Moreover, can you refinance for home improvements?

A cash-out refinance is a low-cost way to make home improvements when you don't have the money on hand. Refinancing can be a good way to borrow a lot of money at once, which means expensive renovations are in reach and won't take much (if anything) from your monthly budget.

Similarly, how do you get money back when you refinance your house? A cash-out refinance is a way to both refinance your mortgage and borrow money at the same time. You refinance your mortgage and receive a check at closing. The balance owed on your new mortgage will be higher than your old one by the amount of that check, plus any closing costs rolled into the loan.

Likewise, should I refinance after remodeling?

If you can qualify for the HomeStyle, it'll likely save you some money and some interest costs. If not, the FHA 203(k) is a good choice, and you can always refinance to a cheaper conventional mortgage a few months (or years) after your renovations are complete.

What is the current interest rate?

Current Mortgage and Refinance Rates

| Product | Interest Rate | APR |

|---|---|---|

| 30-Year Fixed-Rate VA | 3.125% | 3.477% |

| 20-Year Fixed Rate | 3.49% | 3.635% |

| 15-Year Fixed Rate | 3.0% | 3.148% |

| 7/1 ARM | 3.125% | 3.759% |

Related Question Answers

How do you get a loan to renovate a house?

Another way to finance your home renovation is by taking out a home equity loan, also known as a second mortgage. This is a one-time, lump-sum loan, so it's not subject to fluctuating interest rates, and monthly payments remain the same for the loan term. A similar loan is the home equity line of credit, or HELOC.How much equity do I need to refinance?

When it comes to refinancing, a general rule of thumb is that you should have at least a 20 percent equity in the property. However, if your equity is less than 20 percent, and if you have a good credit rating, you may be able to refinance anyway.What is a good interest rate for a home improvement loan?

Using a personal loan for some home improvement projects can be a good idea, depending on your needs and the interest rate you're able to secure. Interest rates on personal loans can range from as low as 2.49% to as high as 36%, however, average rates range from 10.3% to 32%.Can you get a home improvement loan with a new mortgage?

203(k) and HomeStyle Loans: Buy, Renovate With One Mortgage. You'll have more properties to choose from, and you can get a renovation loan that combines the purchase price with the cost of improvements. Two options, FHA 203(k) and Fannie Mae HomeStyle loans, let you borrow money to buy a home and fix it up.Does refinancing hurt your credit?

When you apply to refinance your car, a hard inquiry will be noted on your credit, causing a temporary dip in your score. A car loan refinance also might hurt your credit by reducing the average age of your accounts. That's because your original car loan will be paid off early and replaced by a new auto loan.When should you not refinance?

5 Reasons Not to Refinance Your Mortgage- You're Not Planning on Staying Put. One of the most important details you need to pay attention to when you're planning to refinance is the break-even point.

- Your Credit's Not That Great.

- You Can't Afford the Closing Costs.

- The Long-Term Costs Outweigh Your Savings.

- You Want to Tap Into Your Home's Equity.

Why refinancing is a bad idea?

Refinancing your mortgage can be a good or bad idea, depending on your motivation and goals. Homeowners who refinance can wind up paying more over time because of fees and closing costs, a longer loan term, or a higher interest rate that is tied to a "no cost" mortgage.Is it worth refinancing for .5 percent?

Your new interest rate should be at least . 5 percentage points lower than your current rate. The old rule of thumb was that you should refinance if you could get a rate that was 1 to 2 points lower than your current one.How much does 1 point lower your interest rate?

One point costs 1 percent of your mortgage amount (or $1,000 for every $100,000). Essentially, you pay some interest up front in exchange for a lower interest rate over the life of your loan.When should you refinance your home?

Although every situation is different, I would recommend refinancing your mortgage if:- Current interest rates are at least 1 percent lower than your existing rate.

- You plan on staying in your home for another 5 years (give or take)

- You anticipate being approved for the refinance loan.

Why are refinance rates higher?

The bank can charge a higher interest rate on a refinance because a refinance is a want, not a need, in most cases. This is because you already have a loan in place and the only reasons a borrower would refi is 1) to take out cash or 2) reduce their interest rate (eg.Can you get a bigger mortgage for renovations?

To be able to pay for building works before they are finished, you'll need a specialist renovation mortgage such as those available through Buildstore Mortgage Services. Its Ideal Home Improvement mortgage allows you to borrow up to 95% of the cost of the property as well as up to 95% of the improvement costs.Is a cash out refinance a good idea?

A cash-out refinance can make sense if you can get a good interest rate on the new loan and have a sound use for the money. But seeking a refinance to fund vacations or a new car isn't a good idea, because you'll have little to no return on your money.What happens when you refinance your house?

Refinancing replaces an existing loan with a new loan that pays off the debt of the old loan. You find a lender with better loan terms, and you apply for the new loan. The new loan pays off the existing debt completely. You make payments on the new loan until you pay it off or refinance it.Can you take equity out of your home without refinancing?

Without refinancing your mortgage, there are two ways to borrow against your home equity. You can either take out a home equity loan or a home equity line of credit (HELOC). While they may sound similar, they function very differently.Why would you refinance your home?

There are many reasons why homeowners refinance: to obtain a lower interest rate; to shorten the term of their mortgage; to convert from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage, or vice versa; to tap into home equity to finance a large purchase, or to consolidate debt.What credit score do you need to refinance?

The average minimum credit score for conventional refinancing programs is 620 to 680, although the best rates are generally available to homeowners with scores of 740 or higher. Conventional refinances are always fully documented.What happens to equity when you refinance?

A home-loan refinance may lower your equity in the property. If you're having trouble paying a mortgage, one option is to refinance. This means taking out a new loan with a lower interest rate, which should lower the monthly payment. If you do a "cash-out" refinance, however, your equity will drop.How long does it take to get money from a cash out refinance?

30 to 45 days