31%-40%

Keeping this in consideration, what is the highest DTI for FHA?

57%

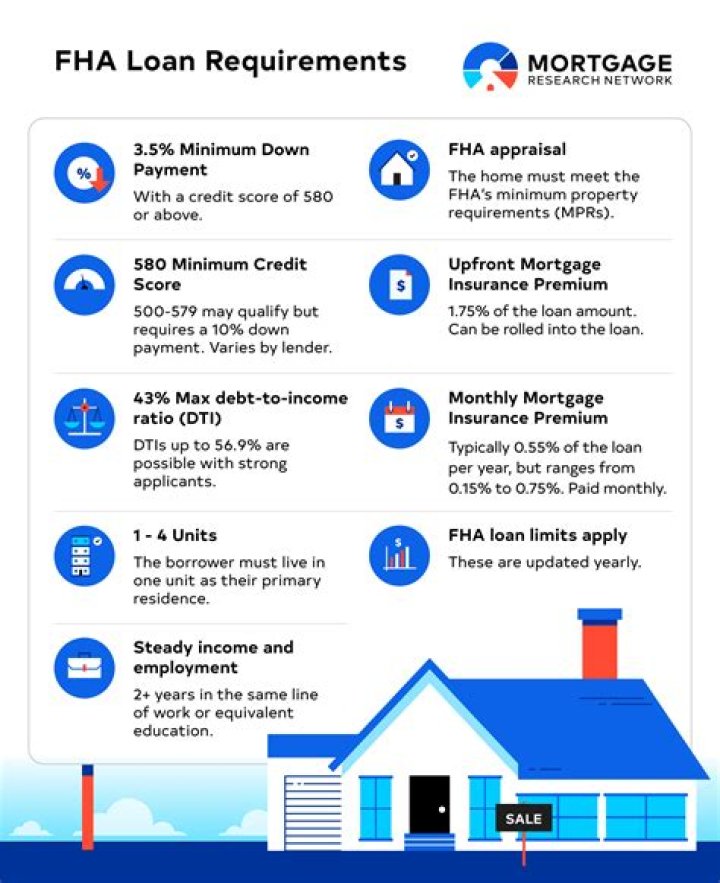

Subsequently, question is, what is included in Front End DTI? The front-end ratio is calculated by dividing an individual's anticipated monthly mortgage payment by his/her monthly gross income. The mortgage payment generally consists of principal, interest, taxes, and mortgage insurance (PITI).

Moreover, what is the max DTI for FHA manual underwrite?

43%

What is the debt to income ratio for FHA loans?

According to the FHA official site, "The FHA allows you to use 31% of your income towards housing costs and 43% towards housing expenses and other long-term debt." Those percentages should be examined side-by-side with the debt-to-income requirements of a conventional home loan.

Related Question Answers

What DTI do lenders look for?

Lenders calculate your debt-to-income ratio by dividing your monthly debt obligations by your pretax, or gross, income. Most lenders look for a ratio of 36% or less, though there are exceptions, which we'll get into below. Debt-to-income ratio is calculated by dividing your monthly debts by your pretax income.”Does FHA allow you to pay off debt to qualify?

FHA and VA mortgage guidelines will allow a borrower to pay down their credit card balances to $0 and the underwriter will only count a $10/month minimum payment towards the borrower's debt to income (DTI) ratio. This is definitely good news for FHA and VA loans.How can I lower my DTI quickly?

How to lower your debt-to-income ratio- Increase the amount you pay monthly toward your debt. Extra payments can help lower your overall debt more quickly.

- Avoid taking on more debt.

- Postpone large purchases so you're using less credit.

- Recalculate your debt-to-income ratio monthly to see if you're making progress.

Do 401k loans count against DTI?

Borrowing From Your 401k Doesn't Count Against Your DTIEven though the 401k loan is a new monthly obligation, lenders don't count that obligation against you when analyzing your debt-to-income ratio. The lender will, however, deduct the available balance of your 401k loan by the amount you borrowed.

Can I get a mortgage with 50 debt to income ratio?

The maximum debt-to-income ratio will vary by mortgage lender, loan program, and investor, but the number generally ranges between 40-50%. However, there is a temporary exemption for many loans, but a lot of lenders still want this number to be under 43%! Get Pre-Approved Today!Can you buy a house with a high debt to income ratio?

Generally, programs get a little more restrictive for DTIs over 36%. You might need a better credit score or bigger down payment to qualify. But most programs will allow a high DTI -- as high as 43% for a well-qualified applicant. And some will let you go as high as 50% with the right compensating factors.Do you include utilities in debt to income ratio?

Calculating your debt-to-income ratioNote that only debt obligations are included in your DTI—not utility bills, phone, cable, or any other regular payments.

What is the max DTI for a conventional loan?

For manually underwritten loans, Fannie Mae's maximum total DTI ratio is 36% of the borrower's stable monthly income. The maximum can be exceeded up to 45% if the borrower meets the credit score and reserve requirements reflected in the Eligibility Matrix.What do FHA underwriters look for approval?

Here are some of the things the FHA underwriter will look for during this process: The borrower's credit scores and (possibly) credit reports. Debt-to-income ratio, or DTI. Bank statements that show current, verified assets.How many FHA mortgage lates can I get?

two

Does FHA use gross or net income?

Calculating 1099 Income for an FHA LoanThey will take that annual total and will divide by 12 to come up with your monthly gross income. Lenders may also take your tax deductions into consideration and may only use the net income. This is what typically makes it difficult to qualify for an FHA loan with 1099 income.

How is front end DTI calculated?

To calculate the front-end DTI, add up your expected housing expenses, and divide it by how much you earn each month before taxes (your gross monthly income). Multiply the result by 100, and that is your front-end DTI ratio.What is the 36 rule?

The rule is simple. When considering a mortgage, make sure your: maximum household expenses won't exceed 28 percent of your gross monthly income; total household debt doesn't exceed more than 36 percent of your gross monthly income (known as your debt-to-income ratio).Does DTI affect interest rate?

A low debt-to-income ratio could have the opposite effect on your interest rate. If your DTI is low enough (either housing or total), you may get a lower interest rate. Lenders prefer borrowers that pose little to no risk of default on their mortgage. If so, you stand a good chance to get a lower rate.How is DTI calculated?

To calculate your debt-to-income ratio, you add up all your monthly debt payments and divide them by your gross monthly income. Your gross monthly income is generally the amount of money you have earned before your taxes and other deductions are taken out.What is a good DTI?

At or below a 36% DTI is considered the ideal ratio to have. 45% is considered a maximum. Although, a much lower DTI is preferred—18%, for example, is considered excellent. And some lenders will accepter a higher ratio.What is a good debt to income ratio to buy a house?

The Ideal Debt-to-Income Ratio for MortgagesWhile 43% is the highest debt-to-income ratio that a homebuyer can have, buyers can benefit from having lower ratios. The ideal debt-to-income ratio for aspiring homeowners is at or below 36%. Of course the lower your debt-to-income ratio, the better.